Think $500 is too small to start earning real passive income?

You can open a brokerage account, buy fractional shares or a dividend ETF, and turn on automatic reinvestment in minutes.

This article shows the exact, low-cost steps to put your $500 to work today, explains what that money is likely to earn (about $10 to $30 a year at common yields), and gives a simple plan to grow those payments over time without chasing risky high payouts.

Immediate Steps to Start Investing $500 for Passive Dividend Income

You can put $500 into dividend assets today by opening a brokerage account with no minimums and zero trading fees. Most modern brokerages let you start with any amount, so your full $500 goes straight to work. No account fees eating into your capital, no per-trade commissions shaving off pieces. Setting up an account takes 10 or 15 minutes online. You’ll need your Social Security number, bank info, and employment details.

Once funded, you can buy fractional shares even when a single share costs hundreds of dollars. That means you can own part of an expensive, high-quality dividend stock without waiting to save up the full share price. Say a stock trades at $300 and yields 4 percent. You invest your $500, own 1.67 shares, and earn dividends on the whole amount. This used to be reserved for bigger accounts, but now it’s standard.

Your $500 will generate somewhere between $10 and $30 a year, depending on yield. Most dividend stocks and ETFs yield 2 to 6 percent annually, paid quarterly. At 3 percent, $500 gives you $15 a year, about $3.75 each quarter. At 6 percent, that’s $30 a year, or $7.50 quarterly. Small numbers at first. But they grow when you reinvest and keep adding capital.

Here’s how to get started:

- Open a brokerage with no minimums and free stock and ETF trades.

- Move $500 from your bank to the brokerage.

- Pick a low-cost dividend ETF or a couple of dividend stocks.

- Turn on the dividend reinvestment plan (DRIP) if available, so dividends buy more shares automatically.

- Check your quarterly payments and watch your share count climb.

Building a Dividend Investing Strategy With Only $500

Choosing what to buy with $500 means weighing yield against safety. A 6 percent stock doubles your income versus a 3 percent position, but higher yields usually signal trouble or stalled growth. Dividends can get cut if earnings drop. High-yielding positions tend to cut more often during downturns. If you go with a diversified ETF yielding 3 to 4 percent, you’re spreading risk across dozens or hundreds of companies, lowering the odds that one cut destroys your income.

Your $500 should focus on long-term compounding, not immediate cash. Even at 6 percent, $500 only delivers $30 a year. That won’t cover anything meaningful. The real value shows up when you reinvest dividends to buy more shares, which then pay their own dividends, year after year. Leave the dividends reinvesting, add fresh money when you can, and your $500 grows into something that eventually generates real monthly income. That shift takes patience, not chasing the fattest yield you can find.

When building your plan, nail down a few basics that fit your risk tolerance:

- Yield range: Stick to 3 to 5 percent. Balances income with dividend stability, avoiding both tiny yields that produce almost nothing and sky-high yields that scream warning signs.

- Position limits: With $500, you’re probably holding one ETF or splitting across two or three stocks. If you add a single stock, cap it at 30 to 40 percent of your total to keep some diversification.

- Reinvestment: Turn on automatic DRIP unless you need the cash right now. Reinvestment speeds up growth.

- Timeline: Plan to hold at least five years. Ride out drops, let compounding work. Short-term dividend investing with $500 produces almost nothing useful.

Choosing Dividend Stocks and ETFs for a $500 Portfolio

Dividend ETFs are the easiest way to start with $500. They bundle dozens or hundreds of dividend companies into one ticker, giving you instant diversification and killing the risk that one company’s cut wipes you out. Take something like the Vanguard High Dividend Yield ETF. Historically yields around 3 percent, holds a broad mix of big, stable dividend payers. Your $500 at 3 percent earns about $15 a year. The fund rebalances itself, drops weak dividend stocks, adds stronger ones. You don’t need to research earnings reports or track individual companies.

If you want to pick individual stocks, focus on companies with long histories of paying and raising dividends, payout ratios below 60 percent (they pay less than 60 percent of earnings as dividends, leaving cushion to sustain or grow payments during tough stretches), and strong, predictable cash flow. Blue chips in consumer staples, utilities, telecoms fit that profile. A utility stock might yield 4 percent, pays quarterly, provides steady income as long as the regulated revenue holds up. With $500, you can grab fractional shares of two or three blue chips, spread risk across industries, still collect quarterly dividends from each.

REITs are another income option, usually yielding 4 percent or higher because they’re legally required to distribute most taxable income to shareholders. A REIT owns apartments, shopping centers, office buildings. Collects rent, covers expenses, sends the rest to investors as dividends, typically quarterly. The 4 percent average means $500 invested generates roughly $20 a year. REITs swing more than dividend stocks because real estate values and occupancy shift around, but they add diversification if your whole portfolio is corporate stocks.

| Asset Type | Typical Yield | Pros | Cons |

|---|---|---|---|

| Dividend ETF | 2%–4% | Instant diversification, minimal research, auto-rebalancing | Lower yield than single high-payers, small management fee |

| Dividend Growth Stock | 2%–3% | Rising dividends over time, blue-chip stability | Lower starting yield, stock picking needed |

| High-Yield Stock | 5%–6%+ | More immediate income per dollar | Higher cut risk, often slower growth |

| REIT | 4%–5% | Real estate exposure, required to pay most income | Interest rate and property market sensitivity |

Using DRIP and Reinvestment to Grow Passive Dividend Income From $500

A dividend reinvestment plan (DRIP) takes each dividend payment and automatically buys more shares of the same stock or ETF, usually with no trading fee. Turn on DRIP for a $500 position yielding 3 percent, and your first quarterly dividend of about $3.75 buys a tiny slice of a new share. That slice earns its own dividend next quarter, which buys another slice. Over years, those bits compound into real growth in both share count and total dividend income. Most brokerages offer DRIP for free, making it an easy set-it-and-forget-it move.

Reinvestment makes a big difference over time. In one scenario, a $10,000 starting position with a 3 percent dividend yield and 5 percent annual price growth ended up roughly 2.5 times bigger when dividends were reinvested versus taken as cash. That extra growth came purely from buying more shares with dividends, then earning dividends on those shares. Same idea applies to $500. It just takes longer to see big jumps because the dollar amounts start smaller.

To get the most from DRIP with your $500:

- Turn on automatic reinvestment in your brokerage settings for each holding.

- Track your share count each quarter. Even a 0.01-share gain adds up.

- Measure annual dividend income year over year. Should rise even without fresh capital, because more shares produce more dividends.

Calculating How Much Passive Income $500 Can Generate

Figuring out expected dividend income is simple. Multiply your investment by the annual yield. Formula: Annual Income = Investment × Yield. Invest $500 at 3 percent? $500 × 0.03 = $15 per year. At 6 percent? $500 × 0.06 = $30 per year. Those numbers are total dividends over 12 months, assuming the payout rate holds steady.

Most stocks and ETFs pay quarterly. Four payments a year. A $500 position at 3 percent yields $15 annually, or about $3.75 every three months. Some companies and REITs pay monthly, smoothing cash flow, but quarterly is standard. Payment schedule doesn’t change total annual income, just when it hits your account. With $500, the quarterly amounts are small enough that most people just reinvest automatically instead of spending the cash.

| Yield | Annual Income on $500 | Monthly Equivalent |

|---|---|---|

| 2% | $10 | ~$0.83 |

| 3% | $15 | ~$1.25 |

| 6% | $30 | ~$2.50 |

Portfolio Diversification With a $500 Dividend Investment

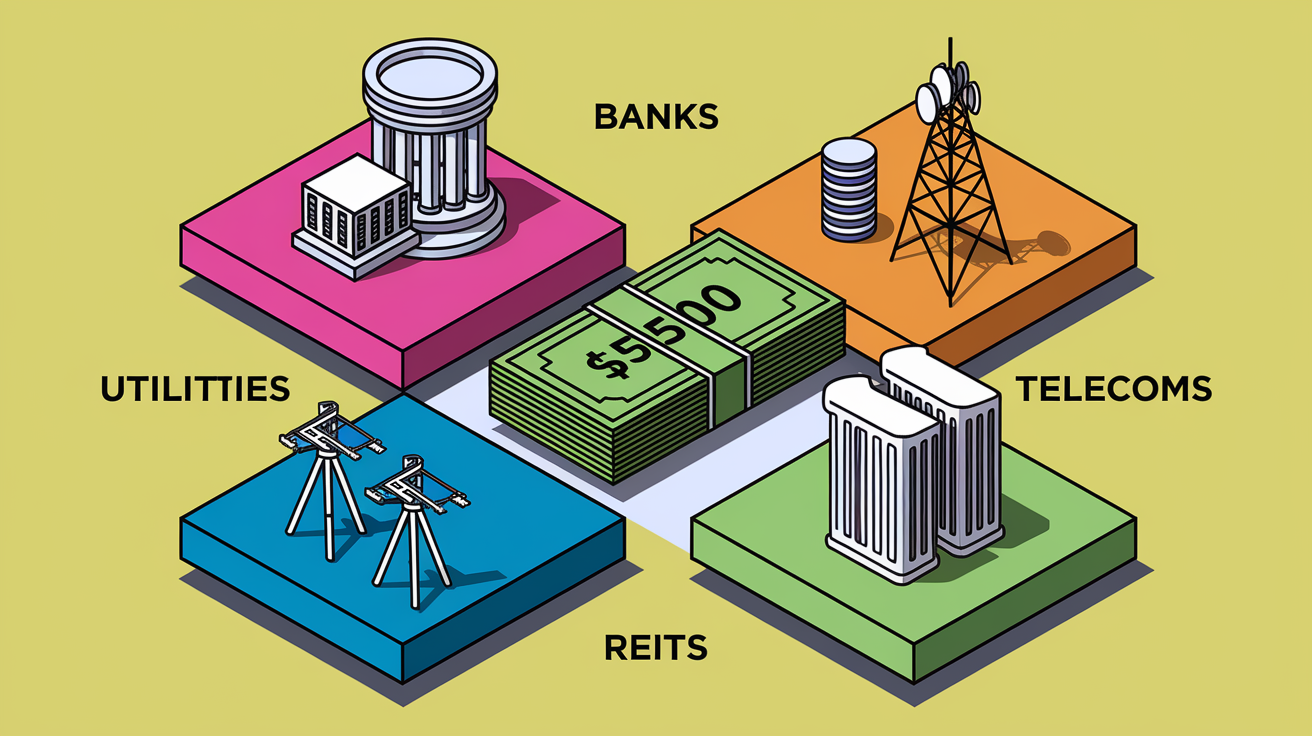

Diversifying with only $500 used to be nearly impossible because buying multiple stocks meant spreading capital so thin that trading fees destroyed your returns. Fractional shares and commission-free trades solved that. You can now split $500 across a dividend ETF and two individual stocks, or dump the whole amount into a single diversified ETF holding hundreds of companies across sectors. An ETF gives you instant exposure to banks, utilities, consumer staples, telecoms, real estate, all in one trade. Kills the risk that a problem in one industry or company tanks your income.

Even a little diversification cuts the chance that a dividend cut or price drop derails everything. Own three stocks and one cuts its dividend in half? You lose about 17 percent of total income if positions were equal-weighted. Own an ETF with 100 holdings and one company cuts? Impact on total dividend is less than 1 percent. During volatility or a recession, some sectors hold up better. Utilities and consumer staples tend to keep paying because people still need power and groceries. Banks and industrials might cut when the economy slows. Spreading $500 across sectors, even through fractional shares, smooths your income.

Four sectors work well for beginners building a small dividend portfolio:

- Banks: Big banks often yield 3 to 4 percent, pay quarterly from steady interest income. Can cut during financial crises but recover.

- Utilities: Electric, water, gas companies provide essential services with regulated revenue, supporting reliable 3 to 5 percent yields and stable dividends.

- Telecoms: Wireless and broadband providers generate recurring subscription revenue, enabling consistent payments in the 4 to 6 percent range.

- REITs: Required to distribute most income, yielding 4 to 5 percent on average. Sensitive to interest rates and property market swings.

Taxes and Accounts for Dividend Income From $500

Dividend income gets taxed, but the rate depends on whether dividends are qualified or ordinary and which account holds the investment. In a regular taxable brokerage, qualified dividends (most U.S. corporations, held for a minimum period) get taxed at the long-term capital gains rate, 0 to 20 percent based on your total income. Ordinary dividends (most REIT distributions, some foreign dividends) get taxed at your regular income rate, same as your paycheck. For $500 producing $15 to $30 a year, the tax bill’s small, maybe $2 to $6, but it still cuts your net income and should factor into your plan.

If you want to skip taxes on dividends entirely and you’re investing long term, open a Roth IRA and buy your dividend stocks or ETFs there. Contributions to a Roth are after-tax dollars, but all dividends, gains, and withdrawals in retirement are completely tax-free if you follow the rules. For a small investor reinvesting every dividend, a Roth lets compounding work without tax drag. One hundred percent of each dividend buys new shares instead of losing a slice to taxes each year. The 2026 Roth contribution limit is $7,000, so your $500 fits easily, and you can keep adding as your income allows.

Final Words

In the action, you learned the quick steps: open a no-minimum, commission-free brokerage, use fractional shares or a dividend ETF, enable DRIP, and review quarterly payouts.

We ran the simple math so expectations stay real, $500 at 3% is about $15 a year, at 6% about $30. Dividends can be cut, so match choices to your timeline and risk comfort.

Follow the five steps in the post and you’ll be moving toward how to invest $500 for passive dividend income with steady, low-stress progress.

FAQ

Q: How much to invest to get $500 per month in dividends?

A: To get $500 per month in dividends you need $6,000 per year; at a 6% yield that’s about $83,333, at 3% about $200,000, and at 2% about $300,000—dividends can be cut.

Q: What is the best investment for $500? What investment can I make with $500? How to turn $500 into more?

A: The best way to invest $500 and turn it into more is to use a commission-free brokerage to buy a diversified dividend ETF or fractional shares, enable DRIP, reinvest earnings, and expect modest income at first.

{kind=link}