What if the smartest investing move isn’t picking hot funds, but choosing the right mix?

Vanguard asset allocation models lay out clear stock, bond, and cash percentages based on your risk level and time horizon.

This post breaks down those typical mixes, conservative, moderate, and aggressive, so you can see the tradeoffs in volatility and returns.

You’ll also get a plain look at Vanguard’s target-date and LifeStrategy frameworks, simple age-based glide paths, and how to pick practical funds to match each mix.

By the end you’ll have a starter plan you can use today.

Core Breakdown of Vanguard Asset Allocation Models for Different Risk Levels

Vanguard’s asset allocation models split your money between stocks, bonds, and cash based on how much risk you’re willing to take and how long you’ve got before you need the money. They give you a starting point. A simple framework that connects your goals to a mix that actually makes sense. Instead of guessing which funds to buy, you pick the mix first, then fill in the rest.

Vanguard builds these models using two tools: the Vanguard Asset Allocation Model (VAAM) and the Vanguard Capital Markets Model®. Both dig into expected returns and how different investments move together, pulling from historical data through December 31, 2024. The goal isn’t to predict where the market’s headed. It’s to hand you a balanced plan that fits your timeline and how much uncertainty you can handle. The models lean toward broadly diversified, low-cost index funds, and they assume you’ll rebalance regularly to stay on track.

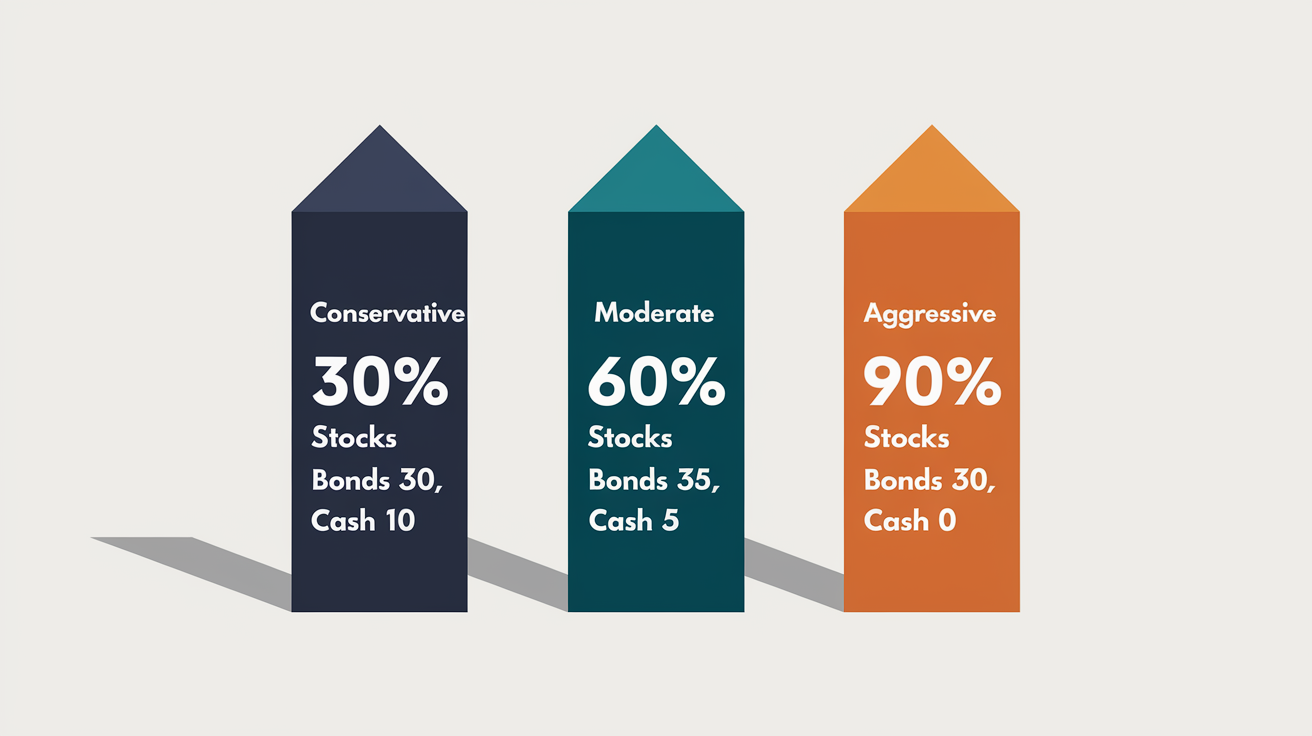

The three examples below show typical stock, bond, and cash splits used in Vanguard-style portfolio construction. They reflect conservative, moderate, and aggressive approaches, so you can compare structure, volatility, and alignment to your personal risk level.

| Model | Stocks % | Bonds % | Cash % |

|---|---|---|---|

| Conservative | 30 | 60 | 10 |

| Moderate | 60 | 35 | 5 |

| Aggressive | 90 | 10 | 0 |

Each model serves a different purpose. Conservative leans on bonds for stability and income. Moderate balances growth with downside protection. Aggressive chases long-term gains and accepts the bumps that come with it.

Understanding Asset Classes in Vanguard Allocation Models

Vanguard blends multiple asset classes to spread risk and capture different types of returns. An investment portfolio is just all the securities you hold. Stocks, bonds, cash, sometimes real estate or commodities. Mixing these together smooths out the ride. When stocks drop, bonds often hold steady or even go up. When inflation spikes, commodities might gain. Diversification doesn’t guarantee profit, but it does reduce the odds that one bad event wipes out your account.

Each asset class plays a role, and each comes with tradeoffs. Knowing what you own and why helps you stick to the plan when markets get loud.

Stocks. Shares of companies. Over the long term, they offer the highest returns, but prices bounce around a lot. You can own stocks directly or through mutual funds and ETFs that bundle hundreds or thousands of companies. High volatility (how much prices swing) is the price you pay for growth.

Bonds. IOUs from companies or governments. They pay regular interest and return your principal at maturity. Bond funds provide income and dampen portfolio swings. The catch is that bond prices fall when interest rates rise, and you face credit risk if the issuer defaults.

Cash and cash-equivalents. Money market funds, stable value investments, checking and savings accounts. These provide stability and quick access to your money. The downside is low growth. Over time, inflation eats into purchasing power, so holding too much cash can cost you.

Real estate. Physical property or funds that invest in real estate (REITs). Adds diversification beyond stocks and bonds, but prices can swing with interest rates, local economies, and tenant demand.

Commodities. Raw materials like oil, gold, and wheat. Can hedge against inflation but add volatility and are tough to hold directly. Most investors access commodities through specialized funds.

Vanguard Model Portfolio Performance Patterns and Historical Behavior

Historical patterns show you what different mixes have done in the past. They can’t predict the future, but they help you understand the range of outcomes. Good years, bad years, and typical long-term returns. Vanguard uses decades of data to model how portfolios behave under stress and during growth. Seeing what a 90/10 mix looked like in 2008 or a 30/60 mix in 1987 gives you a sense of what to expect when markets drop.

Vanguard tracks performance using a chain of indexes that span nearly 100 years. For stocks: the S&P 90 Index from 1926 to March 3, 1957, then the S&P 500 from March 4, 1957 to 1974, the Wilshire 5000 from 1975 to April 22, 2005, the MSCI US Broad Market Index from April 23, 2005 to June 2, 2013, and the CRSP US Total Market Index from then to the present. For bonds: the S&P High Grade Corporate Index from 1926 to 1968, Citigroup High Grade Index from 1969 to 1972, the Lehman Brothers US Long Credit AA Index from 1973 to 1975, the Bloomberg US Aggregate Bond Index from 1976 to 2009, and the Bloomberg US Aggregate Float Adjusted Bond Index from 2010 forward through December 31, 2024.

Diversification lowers risk but never removes it. Even a well-built portfolio can lose value, especially in the short term. The historical record shows four consistent insights.

Volatility differences. An all-stock portfolio swings twice as much as a balanced 60/40 mix. The worst single year for stocks was worse than the worst year for a 50/50 portfolio.

Best and worst year ranges. A 90/10 portfolio might gain 30 percent in a great year and lose 35 percent in a terrible one. A 30/60 portfolio might gain 15 percent and lose 10 percent. The spread narrows as you add bonds.

Long-term return trends. Over 20 or 30 years, higher stock allocations have delivered higher total returns, on average. But those averages hide a lot of year-to-year pain.

Longer horizons smooth outcomes. The range of annual returns is wide. The range of 10-year average returns is much tighter. Time reduces the impact of a single bad year.

How Vanguard Uses Target-Date and LifeStrategy Frameworks Within Allocation Models

Target-date funds follow a glide path, a preset schedule that shifts from stocks to bonds as you get closer to retirement. If you pick a fund with a 2050 target date, it starts aggressive (say, 90 percent stocks) and gradually becomes more conservative. By 2050, it might hold 50 percent stocks and 50 percent bonds. The fund does the rebalancing and the shift for you. One decision, one fund, done.

LifeStrategy funds use a fixed mix that never changes. Vanguard offers four LifeStrategy options: Income (mostly bonds), Conservative Growth (balanced but bond-heavy), Balanced Growth (close to 60/40), and Growth (stock-heavy). You pick the one that fits your risk level today, and it stays put. If you want to get more conservative, you sell one fund and buy another. The difference between target-date and LifeStrategy is automatic drift versus manual control.

| Fund Type | Equity Tilt | Behavior Over Time |

|---|---|---|

| Target-Date Fund | High early, low late | Automatically becomes more conservative as target date approaches |

| LifeStrategy Income | Low (20–30% stocks) | Static mix; no automatic change |

| LifeStrategy Balanced | Moderate (60% stocks) | Static mix; no automatic change |

| LifeStrategy Growth | High (80–90% stocks) | Static mix; no automatic change |

Asset allocation funds offer convenience, but they’re one-size-fits-all. A personalized asset allocation model, built with VAAM and the Vanguard Capital Markets Model®, tailors the mix to your specific goals, timeline, and risk tolerance. You can adjust individual pieces, hold funds across multiple accounts, and rebalance on your own schedule.

Vanguard-Inspired Age-Based Asset Allocation Glide Paths

Age influences how much risk you should take because it tracks your time horizon. A 30-year-old has decades to recover from a market crash. A 65-year-old doesn’t. Two simple rules approximate Vanguard’s lifecycle philosophy: Rule A sets your stock percentage at 100 minus your age. Rule B uses 120 minus your age. Both deliver a glide path that gets more conservative as you get older, but Rule B keeps you more aggressive at every stage.

| Age | Rule A (100 − age) Stocks / Bonds | Rule B (120 − age) Stocks / Bonds | Notes |

|---|---|---|---|

| 30 | 70% / 30% | 90% / 10% | Rule B doubles equity exposure for long-term growth |

| 50 | 50% / 50% | 70% / 30% | Rule B maintains higher growth potential through mid-career |

| 65 | 35% / 65% | 55% / 45% | Rule A leans more conservative; Rule B keeps moderate equity for longevity risk |

Neither rule is perfect. Rule A might leave you too conservative if you expect to live 30 years in retirement. Rule B might feel too risky if a market drop would ruin your retirement timeline. Use the rule as a starting point, then adjust based on your own comfort and goals.

Placement of Vanguard Model Allocations Into Practical Fund Types

Once you know your target percentages, you need to pick the actual funds. Vanguard favors diversified, low-cost index funds because they deliver market returns without the high fees and manager risk that come with active funds. An index fund tracks a benchmark, like the total U.S. stock market or the total bond market, and rebalances automatically as companies enter or exit the index.

Your portfolio typically fills five slots: U.S. equity, international equity, core bonds, intermediate bonds, and cash or money market. Each slot plays a role, and you adjust the size of each slot to match your allocation model.

U.S. equity. A total U.S. stock market fund or a large-cap index fund gives you exposure to thousands of American companies. It delivers growth over the long term and rides out volatility with diversification.

International equity. A total international stock fund spreads your risk outside the U.S. It adds exposure to Europe, Asia, and emerging markets, reducing the impact of a U.S.-specific downturn.

Core bonds. A total bond market fund or an aggregate bond fund holds government and corporate bonds across a range of maturities. It stabilizes your portfolio and generates income, but prices fall when interest rates rise.

Intermediate-term bonds. Shorter duration than core bonds, less sensitive to rate changes. Useful if you want bond exposure with lower volatility.

Cash or money market. A money market fund or stable value fund parks cash safely and keeps it liquid. Returns are low, but you avoid market swings and can access the money quickly.

Passive index funds dominate Vanguard-style allocations because they’re cheap, transparent, and hard to beat over time. Active funds try to pick winners and time the market, but most fail to outperform their index after fees. If you want to add an active fund, keep it small and understand the extra cost and risk.

Rebalancing Within Vanguard Allocation Models

Rebalancing keeps your portfolio aligned with your target mix. When stocks do well, they grow and take up a bigger slice of your portfolio. You end up with more risk than you planned. Rebalancing means selling some of the winners and buying the laggards to restore your original percentages. It feels backward. Selling what’s up and buying what’s down. But it controls risk and enforces discipline.

Vanguard recommends two rebalancing methods: calendar-based and threshold-based. Calendar-based means you check once a year, on a set date, and reset your allocations. Threshold-based means you rebalance anytime an asset class drifts more than a certain amount, usually ±5 percentage points. If your target is 60 percent stocks and they climb to 66 percent, you sell 6 percent to get back to 60.

Annual calendar checks. Pick a date (January 1, your birthday, tax day) and review your allocations every year. Simple and low-stress.

±5 percent threshold. Rebalance only when drift exceeds 5 percentage points. Avoids over-trading in calm markets and acts during big swings.

Use contributions to rebalance. Instead of selling, direct new money to the underweight assets. This avoids triggering taxes in taxable accounts and keeps turnover low.

Turnover and cost considerations. Every trade costs something. A commission, a bid-ask spread, or a tax bill. Rebalance when the benefit (restored risk level) outweighs the cost. Vanguard index funds have low internal turnover, so your rebalancing trades are the main driver of costs.

Example: You start with a 60/35/5 (stocks/bonds/cash) moderate allocation. After a strong year, stocks drift to 66 percent, bonds fall to 30 percent, cash stays at 4 percent. You sell 6 percent of your stock holdings and buy 5 percent bonds and 1 percent cash to restore 60/35/5. Your risk level is back on target.

Vanguard Allocation Models and Investor Scenario Examples

Allocation models change depending on your goal, your timeline, and how much volatility you can stomach. A near-term buyer saving for a house has different needs than a 30-year-old saving for retirement. Vanguard’s six-step process starts with identifying your goal, then matching it to a mix that balances progress and safety.

Time horizon is the biggest lever. Short timelines demand more stability because you can’t afford a 30 percent drop the year before you need the money. Long timelines let you ride out volatility and capture higher long-term returns. Risk tolerance is the second lever. Your emotional comfort with losses and your financial capacity to absorb them. If a 20 percent drop would force you to sell or lose sleep, you need a more conservative mix regardless of your timeline.

The three scenarios below show how goals and timelines shape allocation choices.

Near-term homebuyer (3-year goal). You want to save $10,000 for a down payment. You start with $100 and assume a 6 percent annual return. To hit $10,000 in 3 years, you need to save more than $250 per month. The short timeline means you can’t afford big market swings, so you lean conservative: high cash and short-term bonds, low equity exposure. A 30/60/10 or even 20/70/10 mix keeps your money safe and accessible.

Mid-career retirement saver (10 to 20 years out). You’re 50 years old and plan to retire at 65. You have time to recover from a downturn but not enough to be fully aggressive. A moderate 60/35/5 allocation gives you growth with a cushion. You rebalance annually and gradually shift more conservative as retirement nears.

Long-term retirement saver (30+ years). You’re 30 and retirement is decades away. You can handle volatility because time will smooth it out. A 90/10 aggressive allocation maximizes long-term growth. If the market drops 30 percent, you keep contributing and buy stocks on sale. Example: to reach $10,000 in 6 years starting with $100 and assuming 6 percent annual return, you need to save about $114 per month. The longer timeline and steady contributions let compounding do the heavy lifting.

Final Words

You can now compare a conservative, moderate, or aggressive mix and choose fund types that match your timeline and comfort with ups and downs.

We covered what each model aims to do, how stocks, bonds, and cash behave, where LifeStrategy and target-date funds fit, and why rebalancing matters.

Using vanguard asset allocation models as a guide can help you pick a clear, low-cost mix. They don’t guarantee gains, but they make decisions simpler. If you’re ready, set a target, pick funds, and check once a year – steady progress beats guessing.

FAQ

Q: What are the main Vanguard asset allocation models?

A: The main Vanguard asset allocation models are conservative (30% stocks, 60% bonds, 10% cash), moderate (60% stocks, 35% bonds, 5% cash), and aggressive (90% stocks, 10% bonds, 0% cash). Each model matches a different risk tolerance and timeline.

Q: How does Vanguard determine asset allocation percentages?

A: Vanguard determines asset allocation percentages using the Vanguard Asset Allocation Model (VAAM) and the Vanguard Capital Markets Model, which analyze historical index performance, risk patterns, and long-term return trends to build diversified portfolios aligned with investor goals.

Q: What is the difference between stocks and bonds in Vanguard models?

A: Stocks in Vanguard models offer higher long-term growth but bounce around more, while bonds provide steadier income and cushion drops but carry interest-rate risk. Cash adds stability but loses buying power to inflation over time.

Q: How often should I rebalance a Vanguard allocation model?

A: You should rebalance a Vanguard allocation model once a year or when any asset class drifts more than 5% from your target mix. You can also rebalance by directing new contributions to underweight holdings to avoid selling.

Q: What is a LifeStrategy fund?

A: A LifeStrategy fund is a Vanguard fund with a fixed stock and bond mix that stays the same over time, such as income, balanced, or growth. It is a one-decision portfolio designed for investors who want a set allocation.

Q: How do target-date funds differ from LifeStrategy funds?

A: Target-date funds shift from stocks to bonds as retirement nears following a glide path, while LifeStrategy funds keep the same mix forever. Target-date funds adjust automatically, LifeStrategy funds stay static and require manual rebalancing if your goals change.

Q: What is the 100 minus age rule for asset allocation?

A: The 100 minus age rule for asset allocation means you subtract your age from 100 to get your stock percentage, with the rest in bonds. A 30-year-old would hold 70% stocks and 30% bonds using this simple guideline.

Q: Should I use index funds or ETFs for Vanguard allocation models?

A: You should use index funds or ETFs for Vanguard allocation models because both offer low costs and broad diversification. The choice depends on whether you prefer automatic investing with mutual funds or intraday trading flexibility with ETFs.

Q: How does time horizon affect asset allocation?

A: Time horizon affects asset allocation by allowing longer timelines to handle more stock volatility for higher growth, while shorter timelines need more bonds and cash to protect against market drops you cannot wait out before needing the money.

Q: What happens if I don’t rebalance my portfolio?

A: If you don’t rebalance your portfolio, winning assets grow larger and losing ones shrink, shifting your risk level away from your original plan. A 60/40 mix can drift to 70/30 after a stock rally, increasing volatility beyond your comfort zone.

Q: Can I build a Vanguard-style allocation with any broker?

A: You can build a Vanguard-style allocation with any broker by choosing low-cost index funds or ETFs that track U.S. stocks, international stocks, bonds, and cash. The allocation percentages matter more than the fund company once costs are low.

Q: How do conservative and aggressive models perform differently?

A: Conservative models with more bonds drop less in bad years but grow slower over decades, while aggressive models with more stocks swing harder short-term but tend to deliver higher returns over 20 or 30 years if you stay invested.

{kind=link}