Keeping most of your savings in cash quietly cuts your buying power.

Ready to stop losing ground?

This post walks first-time investors through a simple, low-stress path from cash to an investment plan.

You’ll learn how to size an emergency fund, pick the right accounts, choose a starter mix of low-cost funds, and set an easy timeline to begin.

I’ll also explain the main risks and tradeoffs so you can pick what fits your timeline and nerves.

Immediate Steps to Begin Transitioning Cash Savings Into an Investment Plan

Keeping large amounts of cash in a low-yield savings account quietly shrinks your buying power when inflation runs faster than your interest. If inflation is 3 percent and your account pays 0.5 percent, you lose roughly 2.5 percent of purchasing power each year. Moving excess cash into investments fights that erosion and lets stocks, bonds, and other assets work for you over the long run.

Before you move any money, make sure your emergency fund and short-term needs are covered. Aim for 3 to 6 months of essential expenses in cash, more if your income varies or your job feels risky. Count rent, utilities, food, insurance, minimum debt payments, and transport. If your essentials are $3,000 a month, target $9,000 to $18,000 parked in a high-yield savings or money market account.

Keep money for near-term plans in liquid, low-risk places. If you’ll need the cash within three years for a car, vacation, or down payment, don’t put it into the stock market. Market swings can wipe out value right when you need it. Liquidity protects short-term plans; growth investments play out over a decade or more.

Step-by-step roadmap:

- Add up your cash and monthly essentials, then multiply by 3 to 6 for your emergency target.

- Put that emergency fund in a high-yield savings or money market account and leave it alone unless a real emergency hits.

- If you have an employer 401k match, start there. Then consider a Roth or Traditional IRA if you’re eligible, and a taxable brokerage for extra savings.

- Pick two to four low-cost index funds or ETFs as core holdings.

- Move an initial deposit to your investment account, even $50 to $500 gets you started with many brokers.

- Automate monthly contributions so you invest without thinking about timing the market.

Establishing Clear Investment Goals Before Moving Cash

Decide what you want your money to do before you pick investments. Break goals into short-term (under 3 years), medium-term (3 to 10 years), and long-term (10 years or more). Short-term goals stay in cash or short-term bonds. Medium-term goals get a mix of stocks and bonds. Long-term goals tolerate market ups and downs because you’ve got time to recover.

Be specific. Vague plans like “save for the future” stall you. Use measurable targets with dates and dollar amounts. Want examples? Retirement, a house down payment, college funding, or growing net worth each need different timelines and allocations.

Sample targets:

- Retirement: aim to save around 15 percent of gross income and build enough to replace 70 to 80 percent of pre-retirement income by 65.

- Home down payment: $40,000 in five years could mean $500 a month into a 60/40 stock/bond mix.

- Education: $50,000 over ten years into a 529 or taxable account with steady monthly funding.

- Long-term wealth: reach $500,000 in 20 years by maxing IRA contributions and using employer match.

Assessing Risk Tolerance When Transitioning from Savings to Investing

Risk tolerance is how much volatility you can handle emotionally and financially. Ask yourself: if your $10,000 sank to $7,000 quickly, would you hold, buy more, or sell? Your instincts should guide a realistic stock-to-bond split.

Time horizon matters more than mood. A 25-year-old saving for retirement can take bigger stock bets than someone retiring in ten years. Match risk to the timeline and to your real-life safety net, not to headlines or short-term fears.

Emotional tolerance and financial capacity aren’t the same. Emotional tolerance is how you’d react to losses. Financial capacity is what you can actually afford to lose without derailing bills or plans. A stable job and a year of emergency savings raise your capacity; irregular income and little cash on hand lower it. Balance both when you set your allocation.

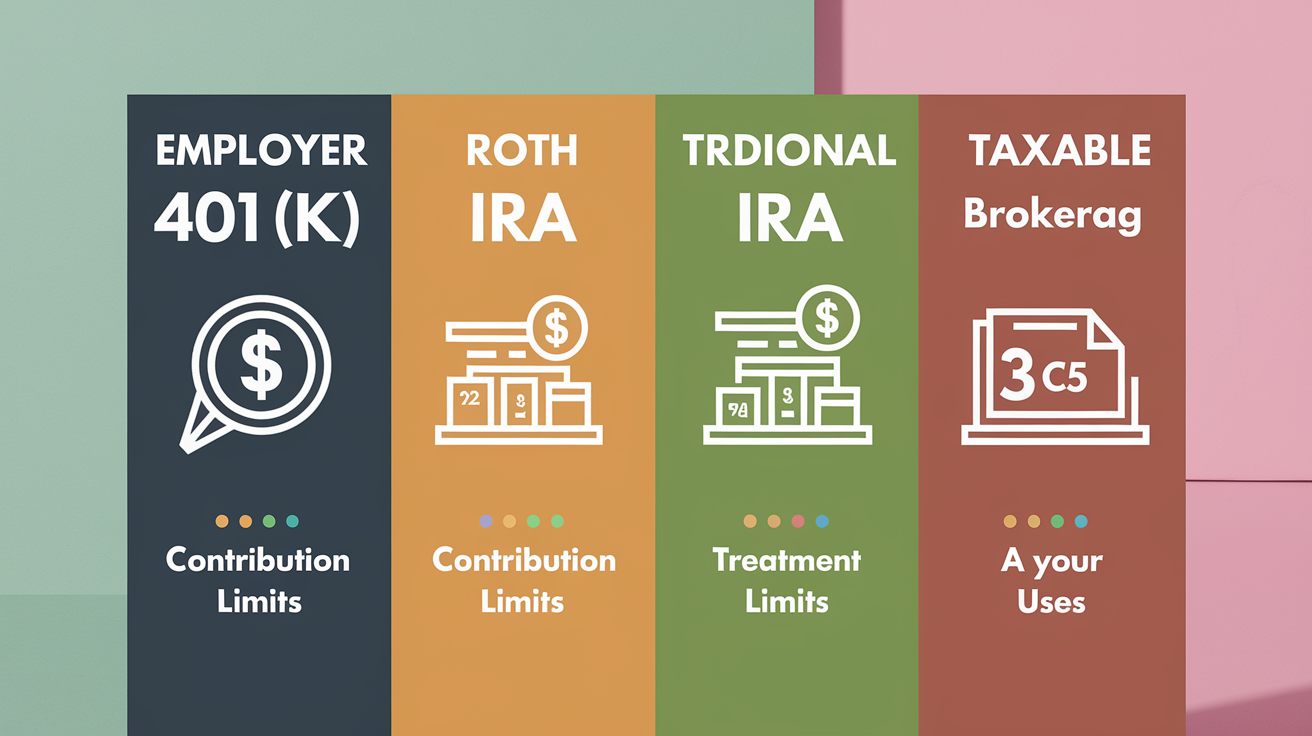

Choosing the Right Accounts for Your First Investment Plan

Account choice determines taxes, contribution limits, and withdrawal rules. Employer 401k plans let you contribute pre-tax dollars and grow tax-deferred. For 2024 the employee deferral limit is $23,000 for under-50s. Always grab the full employer match if available—that’s free money.

IRAs come as Traditional or Roth. Traditional may give a tax deduction now and taxes are paid at withdrawal. Roth accepts after-tax contributions and qualified withdrawals are tax-free. The 2024 IRA contribution limit is $7,000 for those under 50. Check income rules for Roth eligibility.

Taxable brokerage accounts have no contribution limits and offer flexibility, but dividends and capital gains are taxed each year. Use them for goals beyond retirement or after you max tax-advantaged accounts.

| Account Type | Contribution Limits | Tax Treatment | Key Advantages | Typical Use Case |

|---|---|---|---|---|

| Employer 401(k) | $23,000/year (under 50) | Pre-tax contributions, tax-deferred growth, taxed on withdrawal | Employer match, payroll deduction, high limits | Main retirement savings, capture employer match |

| Roth IRA | $7,000/year (under 50) | After-tax contributions, tax-free growth and withdrawals | Tax-free retirement income, no required minimum distributions | Long-term tax-free growth, great for younger savers |

| Traditional IRA | $7,000/year (under 50) | Possible tax deduction, tax-deferred growth, taxed on withdrawal | Potential immediate tax break | Investors expecting lower tax rate in retirement |

| Taxable Brokerage | None | No deduction, dividends and gains taxed annually | Full flexibility, no age or contribution limits | Goals beyond retirement or extra savings |

Investment Vehicles Suitable for First-Time Investors Transitioning from Cash

Start with broad, low-cost funds. A U.S. total stock market fund gives instant, wide diversification. Add an international stock fund for geographic spread and a total bond fund for income and stability. Many of these funds charge 0.03 to 0.20 percent in fees.

If you want hands-off simplicity, consider target-date funds or robo-advisors. They rebalance for you and adjust risk over time. Money market funds and high-yield savings keep cash liquid for short-term goals. CDs lock money for a set term and may penalize early withdrawal.

Quick notes on vehicle types:

- Index funds: track an index, often low minimums and low fees.

- ETFs: trade like stocks, many brokers let you buy fractional shares.

- Mutual funds: can be active or passive; active usually costs more.

- Target-date funds: one-fund solution that shifts allocation over time.

- Bond funds: provide fixed-income exposure and help dampen volatility.

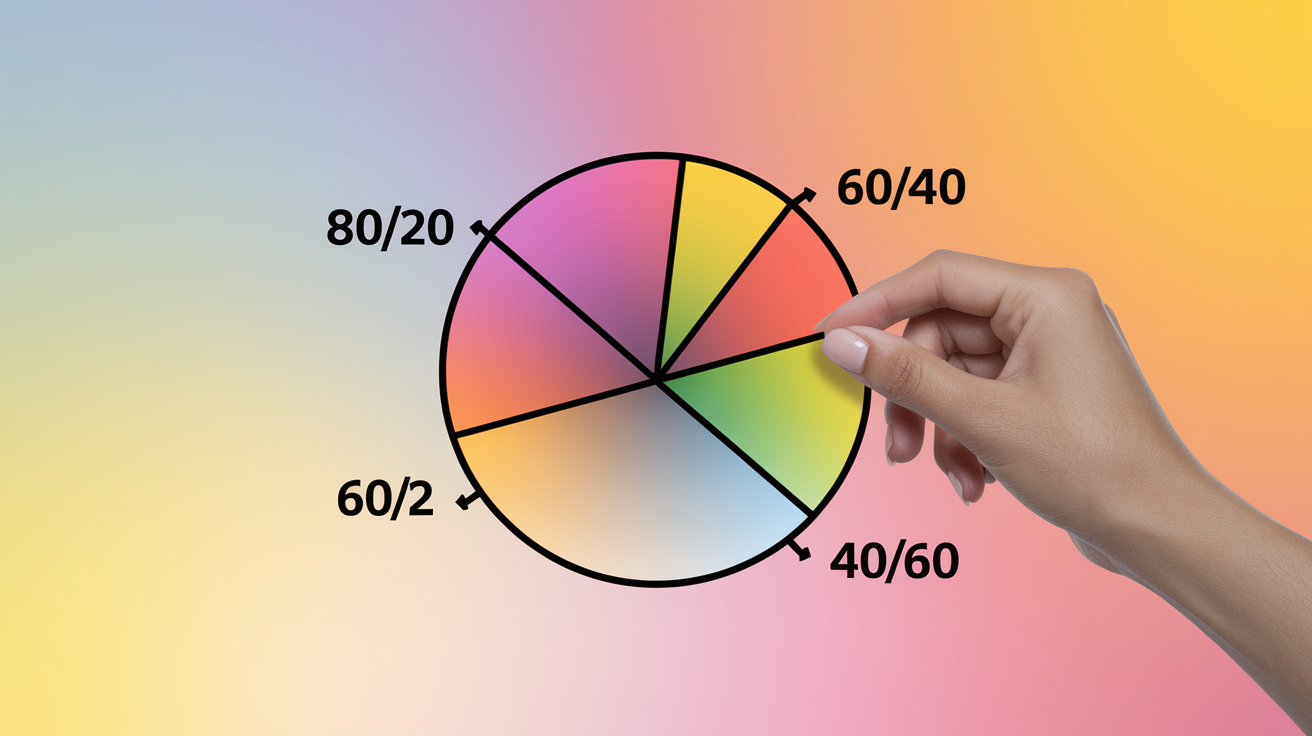

Building a Simple Starter Portfolio When Moving Cash Into the Market

Keep things simple. Pick an allocation that fits your timeline and nerves. Aggressive might be 80 percent stocks, 20 percent bonds. Moderate could be 60/40. Conservative might be 40/60. A common rule of thumb is 100 or 110 minus your age for the percent in stocks, but tweak that based on your situation.

Rebalance when stocks run away and your mix drifts. If your 60/40 drifts to 70/30, sell some stocks and buy bonds to get back to target. You don’t need to rebalance monthly; annual checks or a 5 percentage point drift rule works fine.

Sample three-fund starter:

- U.S. total stock market fund

- International stock index fund

- Total bond market fund

Adjust percentages for aggressive, moderate, or conservative targets and keep the structure simple.

Step-by-Step Timeline for Transitioning from Savings to Investments

Dollar-cost averaging smooths market timing risk. Instead of dumping $10,000 at once, you might invest $1,000 a month for ten months. Automation helps you stay consistent and avoid second-guessing.

Practical timeline:

Days 0 to 30: tally cash, set your emergency target, gather ID and bank details, open your first investment account.

Months 1 to 3: fund 1 to 3 months of expenses, make a starter deposit, pick core funds, and automate monthly transfers.

Months 3 to 12: finish funding 3 to 6 months of expenses, increase contributions as debt falls, lock in your target allocation.

Year 1 and beyond: review annually, rebalance if needed, boost contributions after raises, and make tax-efficient choices when appropriate.

Understanding Fees, Taxes, and Cost Control Before Investing Cash

Fees matter. An extra 0.5 or 1.0 percent in fees quietly cuts decades off your returns. Aim for low expense ratios for core funds and avoid high-cost active managers unless they prove outperformance after fees.

Taxes matter too. Short-term gains (less than a year) are taxed as ordinary income. Long-term gains get lower rates. Use tax-advantaged accounts for long-term compounding and frequent trading when possible. SIPC protects brokerage accounts if a firm fails up to $500,000 including $250,000 for cash, but it won’t save you from market losses. FDIC insurance covers bank deposits up to $250,000 per depositor per bank.

Watch for hidden costs:

- Expense ratios: aim under 0.20 percent for core index funds.

- Trading fees: many brokers offer commission-free ETF trades, but check for mutual fund or maintenance fees.

- Advisory fees: robo-advisors charge around 0.25 percent; human advisors often charge more. Make sure the advice is worth the drag on returns.

- Tax inefficiency: high-turnover funds generate taxable distributions; index funds and ETFs tend to be kinder in taxable accounts.

Monitoring Progress and Rebalancing After Transitioning Cash to Investments

Review once a year and avoid daily balance-watching. Each January or on your birthday, check three things: has your allocation drifted, are contributions on track, and have life changes altered your goals. Rebalance when an asset class drifts about 5 percentage points or on an annual schedule.

If you use target-date funds or a robo-advisor, they’ll handle rebalancing for you. If you manage things yourself, use new contributions to rebalance where possible to limit taxable events in brokerage accounts.

Practical checklist:

- Review statements quarterly to confirm contributions and dividend reinvestment.

- Rebalance annually or at the 5 point drift mark.

- Reassess risk and goals every 3 to 5 years or after major life events.

Avoiding Common Mistakes When Moving from Savings to Investing

Don’t try to time the market. Missing a handful of the best market days can slash long-term returns. Invest consistently instead. Pay down high-interest debt before channeling big sums into the market. A credit card at 18 to 20 percent APR defeats most stock returns.

Always take the employer match. Leaving it on the table is like refusing free money. Avoid chasing hot stocks or sectors and don’t overconcentrate in employer stock. High fees, panic selling during downturns, and investing without an emergency fund are other traps to skip.

Common pitfalls to avoid:

- Investing before building an emergency fund.

- Chasing trends or concentrated bets.

- Paying high fees without clear benefit.

- Selling in panic during bear markets.

- Holding too much employer stock without diversification.

Final Words

Confirm your emergency fund and then take action: set clear goals, check your risk comfort, pick the right account, and choose simple, low-cost funds. Move excess cash in stages and set up automatic transfers so the change happens without daily decisions.

This step-by-step approach shows how to transition from cash savings to an investment plan for first-time investors: assess cash, set goals, pick low-cost index or target-date funds, fund gradually, automate, and review yearly. Stay steady. Small, consistent choices add up.

FAQ

Q: What is the 3 3 3 rule for savings?

A: The 3 3 3 rule for savings is a simple guideline to keep three months of essential expenses in an emergency fund; increase to 6–12 months if your income is variable or job risk is higher.

Q: What is the 7 5 3 1 rule?

A: The 7 5 3 1 rule is not a single standard; different sources use it differently. If you saw it in a plan, check that context. As a safe default, focus on an emergency fund and steady investing.

Q: What is the 3 5 7 rule of investing?

A: The 3 5 7 rule of investing is a rough holding-period guide: treat 3 years as short, 5 as medium, and 7+ as longer-term, which usually supports more stock exposure and riding out market swings.

Q: How much will $10,000 invested be worth in 10 years?

A: How much $10,000 invested will be worth in 10 years depends on annual returns. At 4% it’s about $14,802; 7% ≈ $19,671; 10% ≈ $25,937. Returns are not guaranteed.

{kind=link}