Set-and-forget target date fund or DIY asset mix, which wins for your retirement?

Both can work, but they trade ease for cost and control.

Target date funds handle the heavy lifting, you pick a year and the fund shifts from stocks to bonds.

DIY gives lower fees and better tax placement, but it asks you to check and rebalance a few times a year.

Short version: pick a target date fund if you want almost no work and built-in guardrails.

Pick DIY if you want lower costs and control and you’ll follow a rebalancing plan.

Target Date Funds vs DIY Portfolios: Quick Answer

Target date funds give you a single fund that slowly shifts from stocks to bonds as your retirement year gets closer. You buy it once and the fund company handles the rest. DIY asset allocation means you pick your own mix of stock and bond funds, then rebalance yourself whenever your allocation drifts too far off target.

If you want investing to take ten minutes a year and you don’t mind paying a bit more in fees for convenience, a target date fund is probably your answer. If you want lower costs, more control over exactly where your money goes, and you’re comfortable checking your portfolio a few times a year, DIY makes sense.

Here’s the quick match:

Choose a target date fund if: You’re new to investing, you have one main retirement account, you want zero decisions after the initial purchase, or you worry you’ll panic and sell during a market drop.

Choose DIY allocation if: You want the lowest possible fees, you have multiple accounts and want to place assets tax efficiently, you prefer a custom stock to bond mix, or you’re confident you can stick to a plan when markets get scary.

Key Differences Between Target Date Funds and DIY Asset Allocation

The core structural difference is automation versus manual control. A target date fund follows a preset glide path, meaning the fund’s investment team gradually reduces stock exposure and increases bond exposure as the target retirement year approaches. You never touch it. The fund does the rebalancing, the allocation adjustments, and the decision making. A DIY portfolio starts with allocations you choose, like 60 percent U.S. stocks, 30 percent international stocks, and 10 percent bonds, and you decide when and how to shift that mix over the years.

Customization is another key split. Target date funds assume an average investor retiring in a specific year and build one allocation for everyone in that cohort. DIY portfolios let you tilt more aggressive if you have a pension covering your basics, or more conservative if you plan to retire early and need stability. You can also use DIY to optimize where you hold bonds (in a tax deferred 401(k)) versus stocks (in a taxable brokerage), something a target date fund can’t do because it holds everything in one wrapper.

Volatility control works differently too. The three main contrasts:

Target date funds enforce discipline by locking in the glide path, so you can’t impulsively shift to cash during a crash. DIY portfolios require you to set rules and follow them, like rebalancing once a year or whenever an asset class moves more than 5 percentage points from target. Target date funds can still experience large losses during stock market downturns, because many stay heavily in equities even five or ten years before the target date.

Pros and Cons of Each Strategy

Both approaches work, but each comes with clear tradeoffs depending on your time, knowledge, and priorities.

Target Date Fund:

Pro: Simplicity. You choose one fund based on when you plan to retire and you’re done.

Pro: Automatic rebalancing and glide path adjustments happen without any work from you.

Con: Limited customization. The fund company decides your allocation and you can’t easily adjust for personal circumstances like a pension or high risk tolerance.

Con: Fees can be higher due to fund of funds layering, with some products charging 0.50 percent or more annually.

DIY Portfolio:

Pro: Lower costs if you use broad index funds or ETFs, often under 0.10 percent blended expense ratio.

Pro: Full control over allocation, rebalancing timing, and tax placement across different account types.

Con: Requires ongoing monitoring, discipline to rebalance, and confidence to stick with your plan during market stress.

Con: Risk of behavioral mistakes, like panic selling or chasing hot asset classes, if you lack experience or a clear written plan.

One other practical note: a poorly executed DIY plan can cost you more in missed returns than the fee savings are worth. If you know you’ll second guess every allocation decision or freeze during a downturn, the behavioral guardrails of a target date fund may be the better deal even at a higher expense ratio.

Cost Comparison

Target date funds typically charge an all in expense ratio that covers the management of the fund and the underlying funds it holds. According to industry data, the average target date fund expense ratio sits around 0.51 percent, though some low cost series from Vanguard or Fidelity run closer to 0.08 to 0.15 percent. DIY portfolios cost whatever the individual funds you select charge, and if you stick to total market index funds or ETFs you can build a portfolio with a blended expense ratio under 0.10 percent.

Over decades, a 0.40 percentage point fee difference compounds into real money. On a half million dollar portfolio, that difference costs you about $2,000 per year in extra drag. Over 25 years that drag can reduce your ending balance by tens of thousands of dollars assuming similar gross returns.

| Cost Type | Typical Range | Applies To |

|---|---|---|

| Fund expense ratio | 0.08% – 0.75% | Target date fund |

| Blended fund expenses | 0.03% – 0.20% | DIY portfolio |

| Trading commissions | $0 (most brokers) | Both |

| Advisory or platform fees | 0% – 0.50%+ | Optional, either approach |

Time Commitment and Expertise Needed

Target date funds are designed for investors who don’t want to think about investing more than once. After you choose the fund with a target year close to when you expect to retire, the only ongoing tasks are contributing money and maybe checking your balance once or twice a year to confirm contributions are going through. No rebalancing. No allocation decisions. No research into which bond fund to use. The fund company handles all of that behind the scenes.

DIY portfolios demand more from you. At minimum, you need to understand basic asset allocation concepts, pick three or four broad index funds, and set a rebalancing rule you’ll actually follow. In practice, this might mean spending a few hours upfront researching funds, then 30 to 60 minutes every six or twelve months reviewing your allocations and making trades to bring everything back to target. If your account is large or split across multiple types (taxable brokerage, 401(k), IRA), the complexity grows because you’ll want to locate assets tax efficiently. Bonds in tax deferred accounts and stocks in taxable accounts when possible.

The expertise gap is real. A target date fund doesn’t require you to know what a glide path is or how to calculate a portfolio’s weighted average expense ratio. You just need to pick a reasonable retirement year. DIY requires you to either learn enough to confidently set an allocation and stick to it, or accept that you might make mistakes. If market volatility makes you nervous and you’re not sure how you’ll react to a 30 percent drop, the time you save with a target date fund may be worth more than the fee savings from going DIY.

Risk Management and Rebalancing Differences

Target date funds handle rebalancing automatically on a schedule set by the fund’s investment committee, often quarterly or semi annually. As the fund approaches its target date, the glide path systematically reduces stock exposure and increases bonds and cash. You never have to decide when to sell stocks and buy bonds. The fund does it for you based on the calendar, not on market conditions. This structure prevents you from making emotional timing mistakes, but it also means you can’t pause or adjust the glide path if your personal situation changes.

DIY portfolios put rebalancing responsibility entirely on you. You set the rules. Some investors rebalance once a year on a fixed date, others rebalance whenever an asset class drifts more than 5 percentage points from target, and some combine both methods. The key risk management steps in a DIY approach:

Set clear thresholds. Decide in advance when you’ll rebalance, either by calendar (every 12 months) or by drift threshold (when any holding moves more than 5 percent from target), and write it down.

Stick to the plan during volatility. When stocks drop hard, rebalancing forces you to buy more stocks with proceeds from bonds or cash, which feels uncomfortable but enforces buy low discipline.

Adjust your allocation over time. As you age or approach retirement, manually shift your target allocation to hold more bonds, mimicking a glide path but on your own timeline and risk preference.

The behavioral difference is significant. A target date fund protects you from yourself by removing the rebalancing decision. DIY requires you to act rationally when markets aren’t, which is harder than it sounds but can be managed with rules and a written investment policy.

Who Each Strategy Is Best For

Your situation and preferences will point you toward one method or the other. Target date funds fit hands off investors who value simplicity and want a single decision that covers them through retirement. DIY fits investors who want granular control, lower costs at scale, or the ability to coordinate multiple accounts and tax strategies.

| Investor Type | Recommended Approach | Reason |

|---|---|---|

| New investor, one 401(k) account | Target date fund | Simplicity and built in diversification with zero ongoing effort |

| Experienced investor, comfortable with rebalancing | DIY portfolio | Lower fees and full control over allocation and tax placement |

| Investor with multiple accounts (IRA, 401(k), taxable) | DIY portfolio | Ability to coordinate asset location and optimize taxes across accounts |

| Investor worried about emotional reactions to volatility | Target date fund | Automatic glide path and rebalancing reduce opportunity for panic decisions |

Example Portfolios for Comparison

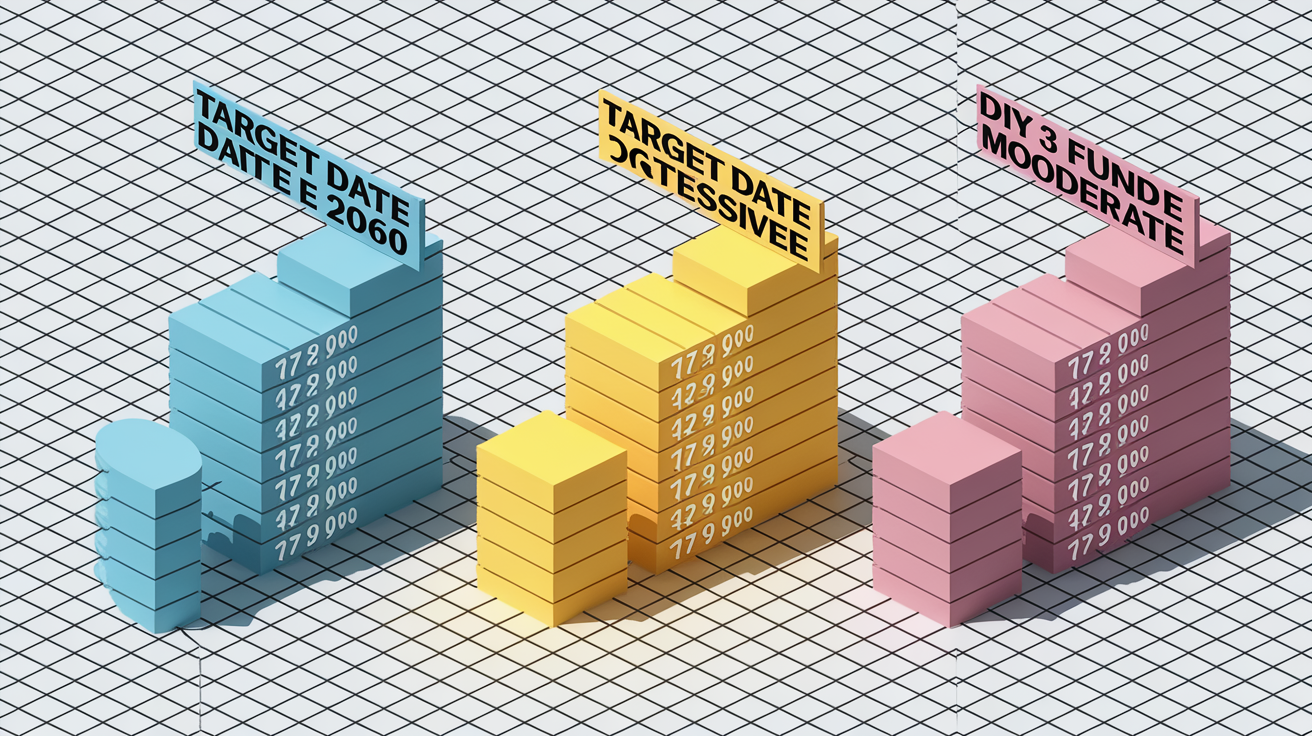

Seeing real allocations helps clarify the difference. A Vanguard Target Retirement 2060 Fund, designed for someone retiring around 2060, holds roughly 90 percent stocks and 10 percent bonds today, split between U.S. and international equities. As the years pass, that fund will automatically reduce stocks and increase bonds according to Vanguard’s published glide path.

| Portfolio Type | Allocation Breakdown | Risk Level |

|---|---|---|

| Target Date 2060 Fund (example) | 54% U.S. stocks, 36% international stocks, 10% bonds | High |

| Target Date 2040 Fund (example) | 49% U.S. stocks, 31% international stocks, 20% bonds | Moderate high |

| DIY 3 fund (aggressive) | 50% VTSAX (U.S. total market), 30% VTIAX (international), 20% VBTLX (U.S. bonds) | Moderate high |

| DIY 3 fund (moderate) | 40% VTSAX, 20% VTIAX, 40% VBTLX | Moderate |

| DIY 2 fund (simple) | 60% VTSAX, 40% VBTLX (no international) | Moderate |

The DIY examples use Vanguard’s total market index funds, which are among the most common low cost building blocks. VTSAX covers about 4,000 U.S. publicly traded companies, VTIAX covers roughly 8,000 international companies, and VBTLX holds more than 10,000 U.S. bonds. You could swap in equivalent ETFs like VTI, VXUS, and BND if you prefer those. The key difference from a target date fund is that you decide the percentages and you manually adjust them as you age or as your risk tolerance changes, giving you flexibility but also responsibility.

Final Words

Compared side-by-side, this post covered how target date funds work, what a DIY asset mix looks like, the cost tradeoffs, time needed, rebalancing differences, and who each approach suits.

Here’s the simple takeaway: target date funds give automatic glide paths and low hassle. DIY gives more control and customization but needs time and know‑how. We showed sample allocations and clear pros and cons to help you decide.

If you’re weighing target date fund vs DIY asset allocation for retirement, pick the approach you’ll stick with. Steady saving and a clear plan win.

FAQ

Q: What’s the quick difference between target date funds and DIY portfolios?

A: The quick difference between target date funds and DIY portfolios is that target date funds automatically shift your mix toward bonds as you near retirement, while DIY gives control but needs decisions and regular monitoring.

Q: How does a target date fund’s glide path differ from DIY rebalancing?

A: A target date fund’s glide path slowly shifts your mix toward bonds on a preset timeline; DIY rebalancing means you pick targets and decide when and how to adjust based on your goals and comfort.

Q: What are the pros and cons of target date funds?

A: The pros of target date funds are simplicity, automatic rebalancing, and low effort; the cons are variable fees, less customization, and a one-size-fits-most approach that might not match your personal risk.

Q: What are the pros and cons of DIY portfolios?

A: DIY portfolios let you customize allocations, choose low-cost funds, and manage taxes; the cons are time, skill needed to rebalance correctly, and a higher chance of emotional mistakes that hurt returns.

Q: Which option typically costs less: target date funds or DIY?

A: Which option typically costs less depends: target date fund expense ratios range about 0.08% to 0.75%; a low-cost DIY three-fund mix plus a cheap platform fee often ends up cheaper.

Q: How much time and expertise does each approach need?

A: How much time and expertise each needs: target date funds need little upkeep; DIY requires learning asset allocation, setting a rebalancing plan, and checking the portfolio periodically—often a few hours per quarter or year.

Q: How do target date funds and DIY portfolios manage risk differently?

A: Target date funds manage risk by automatically moving to more bonds over time; DIY investors must set risk levels and rebalance on a schedule, which gives control but requires discipline to avoid emotional trading.

Q: Who is each strategy best for?

A: Who each strategy is best for: pick a target date fund if you want a hands-off, single choice; pick DIY if you want control, special allocations, or tax moves and can commit time to manage it.

Q: Can you give example allocations for a target date and a DIY portfolio?

A: Example allocations: a 2060 target date fund may be about 90% stocks and 10% bonds; a DIY three-fund example could be 60% US stock, 25% international stock, 15% bonds, offering more tailoring.

{kind=link}